")

It’s a worrying time for the global economy. While the euro area is not yet out of its crisis, and the Fed could trigger an emerging-markets crisis by its imminent rate hike – just remember the “taper tantrum” of 2013 – yet another crisis might happen in China, caused by insolvent shadow banks, bursting asset bubbles, or indebted local governments. The Chinese stock market crash in summer 2015, which sent shock waves around the world, already provided a taste of such a scenario.

What is the likelihood of a financial crisis happening in China, and how would it unfold, domestically and at the global level? Let’s look at China’s main financial risks and efforts to control them, as well as the global effects of a potential crisis in China.

Financial Risks

Today China faces three main risks, which are all routed in the massive stimulus program of 2008: shadow banking, the real estate bubble (or more generally asset bubbles) and private and public debt, especially local government debt. These risks are highly inter-connected and all involve banks, hence the risk of a spill-over to the formal banking sector. What makes things worse for Chinese policymakers is the continuing gradual growth slowdown, measured by GDP and other indicators. With growth rates almost half of what they were 10 years ago, it is no longer possible to grow out of the debt, which was the preferred strategy in the past.

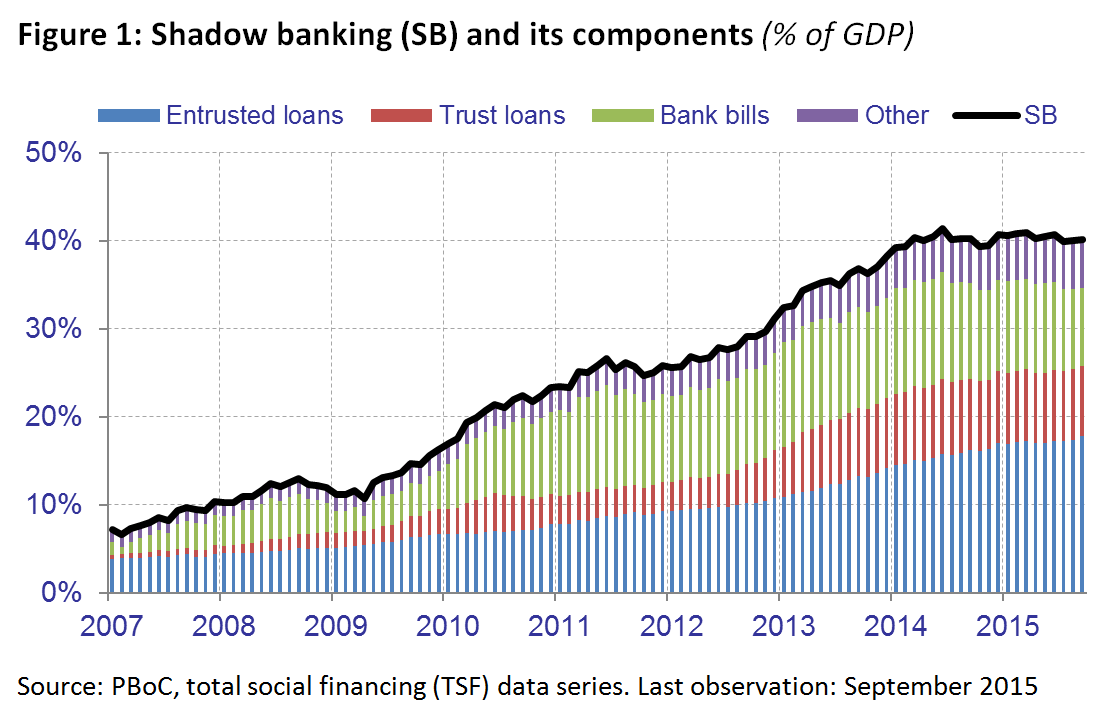

Figure 1 shows the rapid increase of shadow banking activities, which have quadrupled since 2008 to reach 40 percent of GDP, according to the monthly total social financing data published by the People’s Bank of China (PBoC). Using a broader definition of shadow banking, some analysts like JPMorgan estimate its total size up to almost 70 percent of GDP.

Although Chinese shadow banking is not as highly leveraged as the sectors in the U.S. and Europe, it is also insufficiently regulated and carries considerable credit and liquidity risks. Shadow banks are using the funds raised through the issuance of wealth management products to provide loans to local governments and real-estate developers, thereby fueling the Chinese real estate bubble. While authorities have partly been successful in curbing real estate speculation (via higher down-payments, for example) and in reducing the country’s reliance on real estate development to drive growth, a sizeable property bubble remains, which still leads to oversupply in the form of ghost cities.

The level and pace of increase of private and public indebtedness is just as worrying. Quoting a McKinsey report, according to which China’s total debt – accumulated by private households and firms as well as central and local government – rose from 158 perent of GDP in 2007 to 282 percent in 2014 (“among the world’s highest for a major economy”), Chen Zhiwu commented on China’s dangerous debt in Foreign Affairs: “If China doesn’t get on top of its debt problem, the road ahead will be far bumpier than it was in 2008 and could even lead to a prolonged and painful crash.” Of particular concern is the maturity mismatch between short-term debt and long-term investments of local governments, which increases repayment burdens and amplifies the credit risk.

Counter-measures

China’s top leadership under Xi Jinping seems to be aware of the severity of these risks, as it has stepped up the reform of the outdated fiscal and tax system, an important root cause, and also taken other measures. While observers often deplore the slow implementation of the Third Plenum agenda, fiscal reforms are in fact an area where a lot of progress has taken place, as pointed out by Barry Naughton.

In June 2014, Xi’s “Leading Group on Comprehensively Deepening Reform ” approved a bold fiscal reform program, and a long-awaited new Budget Law was adopted in August 2014, which took effect on January 1, 2015. For the first time, it allows local governments to issue bonds to finance their investments, and puts their budgets under closer scrutiny. At the National People’s Congress (NPC) in March 2015, Minister of Finance Lou Jiwei held a press conference to explain the fiscal reforms, which the dedicated government website calls a “breakthrough of deepening reform” (China has really arrived in the present – even the highest officials know how to sell their work). The expansion of the local government debt swap program in the third quarter of 2015 to 3.2 trillion yuan ($503 billion) is also encouraging, even if this equals only 13 percent of the total local government debt, which was 24 trillion yuan ($3.76 trillion) at the end of 2014, including 15.4 trillion in direct debt and 8.6 trillion contingent debt.

Equally important are two other policy measures, which address the moral hazard problem and the risks in the shadow-banking sector. On May 1, 2015, a deposit insurance scheme was introduced, which removes the implicit state guarantee for China’s state-owned banks, and on October 23, 2015, the People’s Bank of China fully liberalized interest rates by removing the deposit rate cap. This is an important step, as the cap drove many investors into higher-yielding but riskier shadow-banking products (see also Sara Hsu’s comment in The Diplomat). The full interest rate liberalization was first announced by PboC Governor Zhou Xiaochuan at the National People’s Congress in March 2014, who said it would “happen within the next 1-2 years.” The move allows rates to fully reflect risks and reduces the funding supply of the shadow-banking system.

An area with less progress is the crucial reform of state-owned enterprises (SOEs). They account for a large part of the corporate debt, and their notoriously low profitability increases the probability that loans to SOEs default. Non-performing loans at commercial banks are already rising fast and stood at 1.7 percent of GDP in June 2015, compared to 0.9 percent in 2012.

Crisis Scenarios

While the reform efforts go in the right direction, the big question is whether they will be enough, whether they are implementable against vested interests, and whether they are sustainable under the growing pressure for China’s leaders to deliver growth, which is needed to maintain their legitimacy and avoid social unrest. Although the reforms help to sustain growth in the long run, they take a toll on it in the short run and could therefore always be reversed. Furthermore, the stock market fiasco has damaged the credibility of Chinese policymakers and of the reform process as a whole.

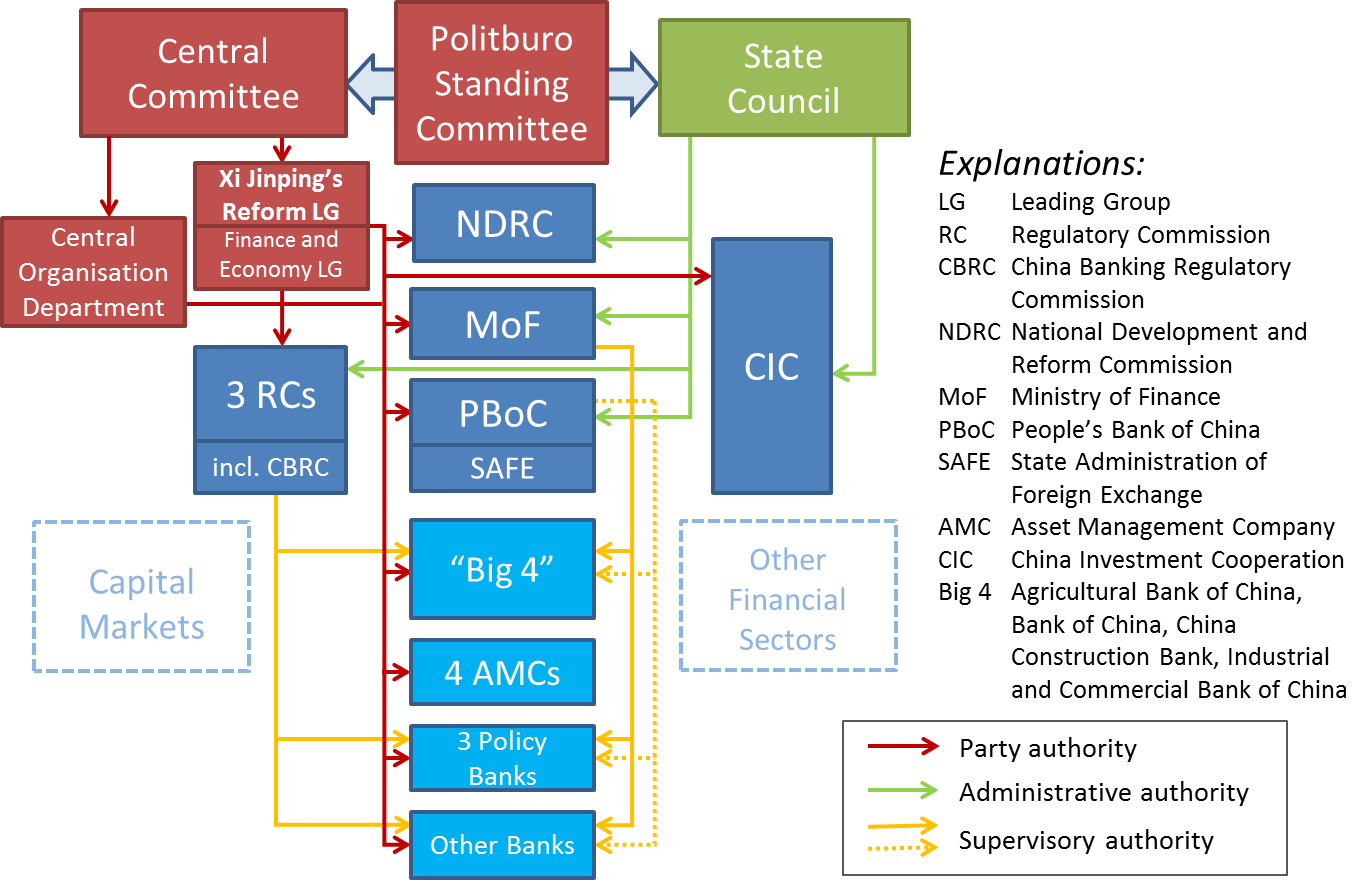

A Chinese crisis would not look like a normal panic, thanks to the tight control of the Communist Party over the financial system (see Figure 2) and over the in- and outflows of capital. Instead, it might start with falling property prices and hence trouble for shaky shadow banks, as real estate is used as collateral for loans. Local governments would be hit as land sales are an important part of their revenues. The combined effect would be a sharp growth slowdown, as real estate construction and infrastructure investments by local governments are key sources of Chinese demand.

With China as one of the world’s most important economic engines, the growth shock would be felt globally via three transmission channels: direct and indirect trade effects, business confidence effects, and lower commodity prices resulting from lower commodity demand. The latter would affect commodity exporters, while the trade effects would most affect the Asian neighbors closely linked to China: Japan, Korea, and Taiwan as well as the ASEAN countries. Europe and the U.S. would also be impacted, although to a lesser extent. The European Central Bank, for example, has calculated that direct and indirect trade effects from a 1 percent slowdown in Chinese real GDP would cause a decrease in euro area activity of around 0.1 to 0.15 percent after two to three years. In addition, uncertainty would spill over into global equity markets, as the recent stock market turmoil has clearly shown. The ECB notes that “the impact […] of a potential further slowdown in China ultimately hinges on the extent to which this slowdown spills over to other emerging markets more generally, and the degree to which the resulting loss of confidence affects global financial markets as well as global trade.”

To conclude, a domestic financial crisis is not unlikely to happen in China, and very likely to spread globally, should it indeed happen. To implement all the reforms necessary to avert a Chinese crisis is almost a “mission impossible,” or at least very difficult in the complex Chinese policymaking context, which involves a high degree of institutional overlap, conflicting goals and interests, and political bargaining. Even such a strong leader like Xi Jinping cannot change this context, and it is not even clear how high financial risks are on his agenda. The centralization of the reforms on Xi himself, coupled with his far-reaching anti-corruption campaign, might also cause inertia among local officials, which are urgently needed to make the fiscal and financial reforms a success.

Western central banks increasingly refer to China when revising down their outlook and justifying monetary policy decisions, but maybe the West in general could do more to support China in its complex reform process, thus helping to avoid that global uncertainty and instability emanate from China in the first place. A China that succeeds in its reforms is far preferable to a China that fails.

Patrick Hess is a senior financial market and China expert working at the European Central Bank. The views expressed here are entirely his own.